An emergency fund is not a luxury — it’s financial survival insurance.

Without it, one unexpected car repair, medical bill, or job loss can force you into debt and undo years of progress. Yet most people struggle to save because they believe they “don’t have enough money left at the end of the month.”

The truth is: you don’t need a high income to build a solid emergency fund. You just need the right system and consistency.

Here’s a realistic, step-by-step plan that works even if you’re currently living paycheck to paycheck.

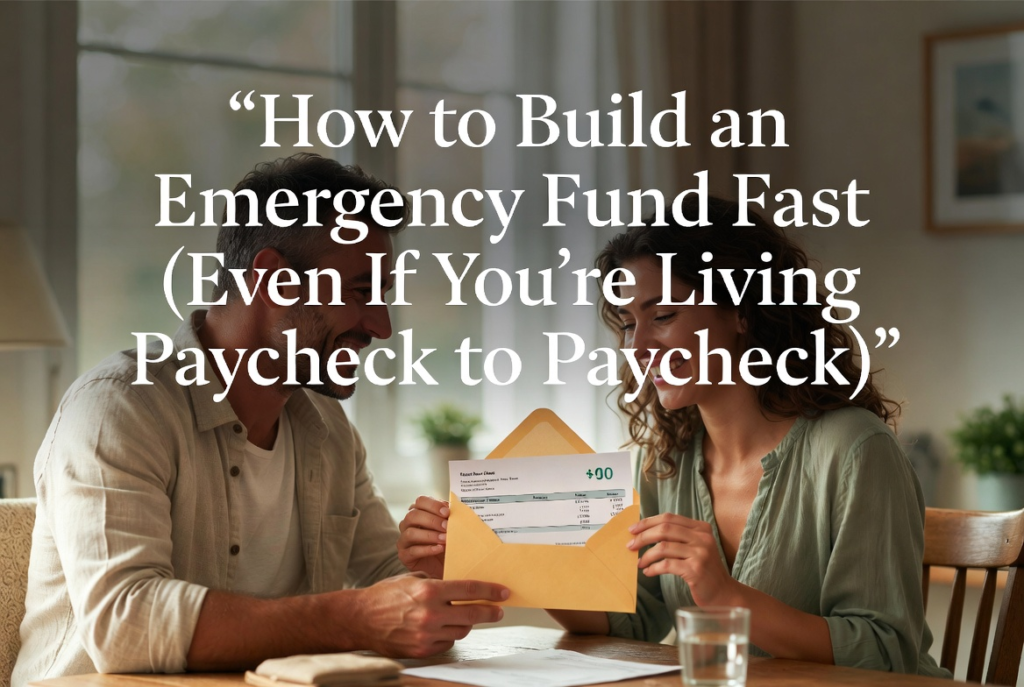

Step 1: Define Your Real Emergency Fund Goal

Forget the old “3–6 months of expenses” rule for now. Start smaller and more achievable:

- Beginner Goal: $1,000 (your first safety net)

- Intermediate Goal: 1 month of essential expenses

- Full Goal: 3–6 months of essential expenses

Essential expenses = housing, food, utilities, transportation, minimum debt payments. Not your full lifestyle.

Step 2: Find “Hidden” Money in Your Current Budget

Even on a tight budget, most people can free up $100–300 per month by making small changes:

- Cancel unused subscriptions (average person has $200+/month in forgotten ones)

- Reduce eating out by half

- Negotiate bills (insurance, phone, internet)

- Sell items you no longer use

- Switch to cheaper alternatives for groceries and household items

Every $50 you cut becomes $600 per year toward your emergency fund.

Step 3: Use the “Pay Yourself First” Rule (Reversed)

Instead of saving what’s left at the end of the month, take the savings out first — the day you get paid.

Practical system:

- Open a separate savings account (preferably at a different bank so it’s not easy to spend)

- Set up an automatic transfer the same day your salary hits your account

- Start with whatever you can afford: $25, $50, or $100 per paycheck

Even $50 per week = $2,600 in one year.

Step 4: Speed Up Your Emergency Fund with These Tactics

- The 30-Day Challenge For one month, track every single dollar you spend. You’ll naturally spend less.

- Windfall Rule Any unexpected money (tax refunds, bonuses, gifts, overtime) goes 50–100% straight into your emergency fund.

- Side Income Rule Any extra money you earn from side work goes directly to the emergency fund until you reach your first $1,000.

- Round-Up Savings Round up every purchase to the nearest dollar and send the difference to savings.

Step 5: Protect and Maintain Your Fund

- Never use the emergency fund for non-emergencies (vacations, new phones, etc.)

- If you have to use it, make replenishing it your top priority

- Once you hit your full goal, shift extra savings toward investments or debt payoff

Real Results People Are Getting

Families following this approach typically:

- Reach their first $1,000 in 3–6 months

- Build a full 3-month emergency fund in 12–24 months

- Feel significantly less financial anxiety

- Stop relying on credit cards for emergencies

Final Encouragement

Building an emergency fund is one of the most loving things you can do for yourself and your family. It’s not about being rich — it’s about buying peace of mind.

Start today with whatever you can:

- Open that separate savings account

- Set up your first automatic transfer (even if it’s only $20)

- Commit to not touching it unless it’s a real emergency

You don’t need a perfect income. You just need to start.

Have you tried building an emergency fund before? How far did you get, and what stopped you?

Share your experience in the comments — your story can motivate others who feel stuck.

For more practical money guides, check out our articles on creating a bulletproof budget, paying off debt fast, and building generational wealth right here on Next Future Finance.

Your emergency fund — and your financial peace — starts with one small decision today.

Deja una respuesta