Debt doesn’t have to control your life.

Whether it’s credit cards, student loans, a car loan, or personal debt — many people feel stuck, stressed, and ashamed. The good news is that you can pay off debt much faster than you think without living like a monk or giving up everything you enjoy.

Here’s a realistic, proven strategy that thousands of families are using successfully right now.

Step 1: Face the Truth (Stop Avoiding It)

The first and most important step is knowing exactly how much you owe.

Make a simple list with:

- Creditor name

- Total balance

- Interest rate

- Minimum monthly payment

Be honest. Many people are shocked when they see the total number for the first time.

Pro Tip: Use a free spreadsheet or even a piece of paper. No fancy apps needed.

Step 2: Choose Your Debt Payoff Strategy

There are two powerful methods. Choose the one that motivates you most:

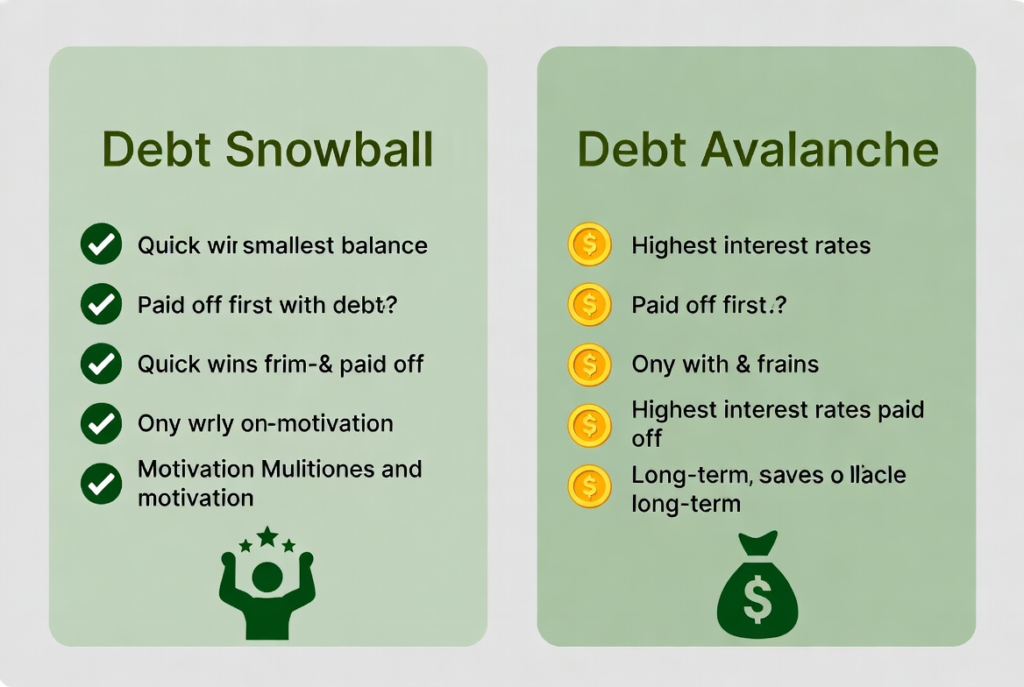

A. The Debt Snowball Method (Best for motivation)

Pay off your smallest debts first, regardless of interest rate. Every time you pay off one debt, you roll that payment into the next one. The quick wins keep you motivated.

B. The Debt Avalanche Method (Best for saving money)

Pay off the debts with the highest interest rate first. This saves you the most money in interest over time.

Recommendation: Use Snowball if you need motivation. Use Avalanche if you want to save the maximum amount of money.

Step 3: Free Up Money to Attack Your Debt

Here are the fastest ways to create extra money each month:

- The 24-Hour Rule Wait 24 hours before any non-essential purchase over $30.

- Cut the “Invisible” Expenses Subscriptions, eating out, impulse shopping, and small daily habits (coffee, snacks, etc.).

- Increase Your Income Even an extra $200–400 per month from a side hustle, overtime, or selling unused items makes a huge difference.

- Negotiate Your Bills Call your internet, phone, insurance, and cable providers. Many people save $30–100 per month just by asking.

Step 4: Create Your “Debt Destroyer” Payment Plan

Example:

- You have $800 extra per month after covering essentials.

- You have 4 debts totaling $18,000.

Using the Snowball method:

- Pay minimums on all debts

- Put the entire $800 extra toward the smallest debt

- When that debt is gone, roll the full payment to the next one

Most people using this method aggressively can become debt-free in 2–4 years instead of 10–20 years.

Step 5: Protect Your Progress (Don’t Fall Back)

- Build a small emergency fund ($1,000) before attacking debt aggressively

- Celebrate milestones (without spending money)

- Review your progress every month

- Never add new debt while paying off old debt

Real-Life Results

Families following this approach consistently report:

- Becoming debt-free in under 3 years

- Huge reduction in monthly stress

- More money available for savings and fun once the debt is gone

- Better relationships (money fights decrease dramatically)

Final Motivation

Paying off debt is not about punishment. It’s about buying back your freedom.

Every extra payment you make is buying back your future — more choices, less stress, and more peace.

Start this week:

- Make your debt list

- Choose your strategy (Snowball or Avalanche)

- Find at least $100–200 extra per month to attack your smallest debt

You don’t need to be perfect. You just need to start and stay consistent.

Have you tried paying off debt before? What worked for you and what didn’t?

Share your story in the comments — your experience can inspire someone else who is struggling right now.

For more practical finance guides, check out our articles on creating a bulletproof budget, building generational wealth, and how to create passive income right here on Next Future Finance.

Your debt-free life is closer than you think.

Deja una respuesta