Inflation in 2026 continues to pressure household budgets. With prices for food, energy, and housing rising faster than many salaries, building savings feels harder than ever. However, it’s still very possible to grow your savings quickly — even in a high-inflation environment.

- 1. Shift Your Mindset: Savings First, Not Whatever Is Left

- 2. Open the Right Type of Savings Account

- 3. Create an Inflation-Adjusted Budget

- 4. Aggressively Cut High-Impact Expenses

- 5. Boost Your Income to Accelerate Savings

- 6. Protect and Grow Your Savings

- 7. Track Progress and Adjust Monthly

- Final Thoughts: You Can Build Savings Rapidly — Start This Week

This step-by-step guide gives you clear, practical actions you can start today to build savings rapidly without needing a massive income or living like a hermit.

1. Shift Your Mindset: Savings First, Not Whatever Is Left

The biggest mistake most people make during inflation is trying to save “whatever is left” at the end of the month. In a high-inflation world, that usually means nothing is left.

Step 1: Adopt the “Pay Yourself First” rule. As soon as your paycheck hits your account, automatically transfer a fixed amount (even if it’s just $50–100 at the beginning) into a separate savings account.

This simple change turns saving into a priority instead of an afterthought.

2. Open the Right Type of Savings Account

Keeping money in a traditional bank account paying 0.01%–0.5% interest while inflation is at 3%+ means you’re quietly losing purchasing power.

Step 2: Move your savings to a high-yield savings account (HYSA). In 2026, many online banks still offer rates between 4% and 5% APY. This helps your money grow faster and partially offsets inflation.

Also consider:

- Money market accounts for slightly better liquidity

- Short-term CDs if you won’t need the money for 6–12 months

Pro tip: Set up automatic recurring transfers so the money moves before you can spend it.

3. Create an Inflation-Adjusted Budget

A budget that doesn’t account for rising prices quickly becomes useless.

Step 3: Build a realistic zero-based budget.

Try this adjusted version of the 50/30/20 rule during high inflation:

- 60–65% Needs (rent, groceries, utilities, transport)

- 15–20% Wants (entertainment, dining out)

- 20–25% Savings & Debt repayment

Track your spending for at least two weeks using a simple app or spreadsheet. Identify your biggest “inflation victims” — usually groceries, gas, and utilities — and create specific reduction targets for each.

4. Aggressively Cut High-Impact Expenses

Focus your energy on the categories where you can save the most money fastest:

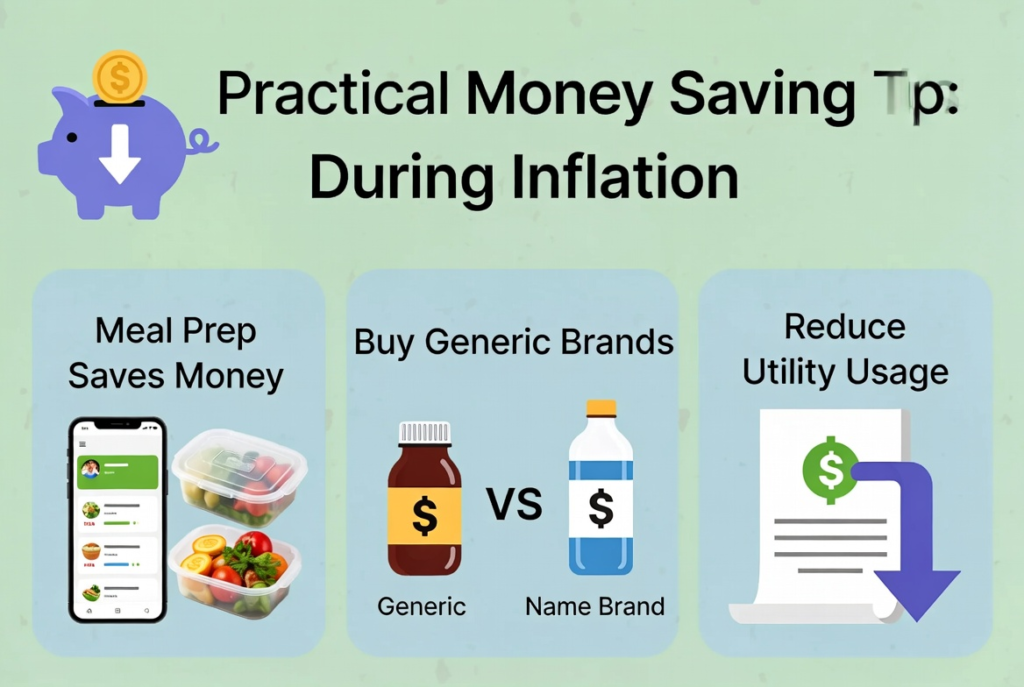

- Groceries & Food: Meal plan weekly, buy in bulk for staples, choose store brands, and reduce eating out. Many people save $150–300/month with this alone.

- Subscriptions: Cancel or pause everything you haven’t used in the last 30 days.

- Transportation: Combine errands, use public transport or carpool when possible, and maintain your car to avoid expensive repairs.

- Housing & Utilities: Negotiate rent if possible, lower thermostat by 1–2 degrees, and fix any energy leaks.

5. Boost Your Income to Accelerate Savings

Cutting expenses gets you part of the way — increasing income gets you there much faster.

Step 5: Add a side income stream.

Easy options for beginners in 2026:

- Sell unused items online (clothes, electronics, furniture)

- Offer services you already know (tutoring, graphic design, pet sitting, rideshare)

- Take on weekend or evening gigs

- Ask for a raise or look for better-paying opportunities

Even an extra $200–500 per month can dramatically speed up how quickly your savings grow.

6. Protect and Grow Your Savings

Once you start building momentum, protect what you’ve saved:

- Build a proper emergency fund first (3–6 months of essential expenses)

- Pay down high-interest debt (credit cards above 15–20% should be prioritized)

- For money you won’t need in the next 3–5 years, consider low-cost index funds or ETFs that historically outpace inflation over time

Avoid speculative investments when trying to build savings rapidly — consistency beats chasing high returns.

7. Track Progress and Adjust Monthly

Step 7: Review your savings every month.

Ask yourself:

- How much did I save this month?

- Which strategies worked best?

- What needs to be adjusted because of new price increases?

Celebrate small wins (every $500 or $1,000 milestone) to stay motivated. Use visual trackers or savings apps that show your progress — seeing the balance grow is incredibly motivating.

Final Thoughts: You Can Build Savings Rapidly — Start This Week

High inflation makes saving feel harder, but the people who succeed are those who take consistent, deliberate action instead of waiting for the economy to improve.

Start with just one or two steps this week:

- Open a high-yield savings account

- Set up your first automatic transfer

- Create a simple budget

Small actions repeated over time create massive results. Many readers who follow this exact approach report building $2,000–$5,000 in savings within 4–6 months, even during challenging economic times.

Inflation is temporary. The savings habits you build now will benefit you for years to come.

You’ve got this.