Investing used to require either hiring a financial advisor at significant cost or doing everything yourself with very little guidance. Robo-advisors changed that. They brought automated, low-cost portfolio management to anyone with a smartphone and a few hundred dollars.

- What Is a Robo-Advisor?

- How Does a Robo-Advisor Actually Work?

- Robo-Advisor vs Human Financial Advisor: Key Differences

- The Main Advantages of Robo-Advisors

- The Limitations of Robo-Advisors

- Leading Robo-Advisors in 2026: A Comparison

- Who Should Use a Robo-Advisor?

- Who Should NOT Use a Robo-Advisor?

- Frequently Asked Questions

- Key Takeaways

But what exactly is a robo-advisor, how does the technology actually work, and is it the right choice for your situation? This guide answers all of those questions plainly and honestly.

What Is a Robo-Advisor?

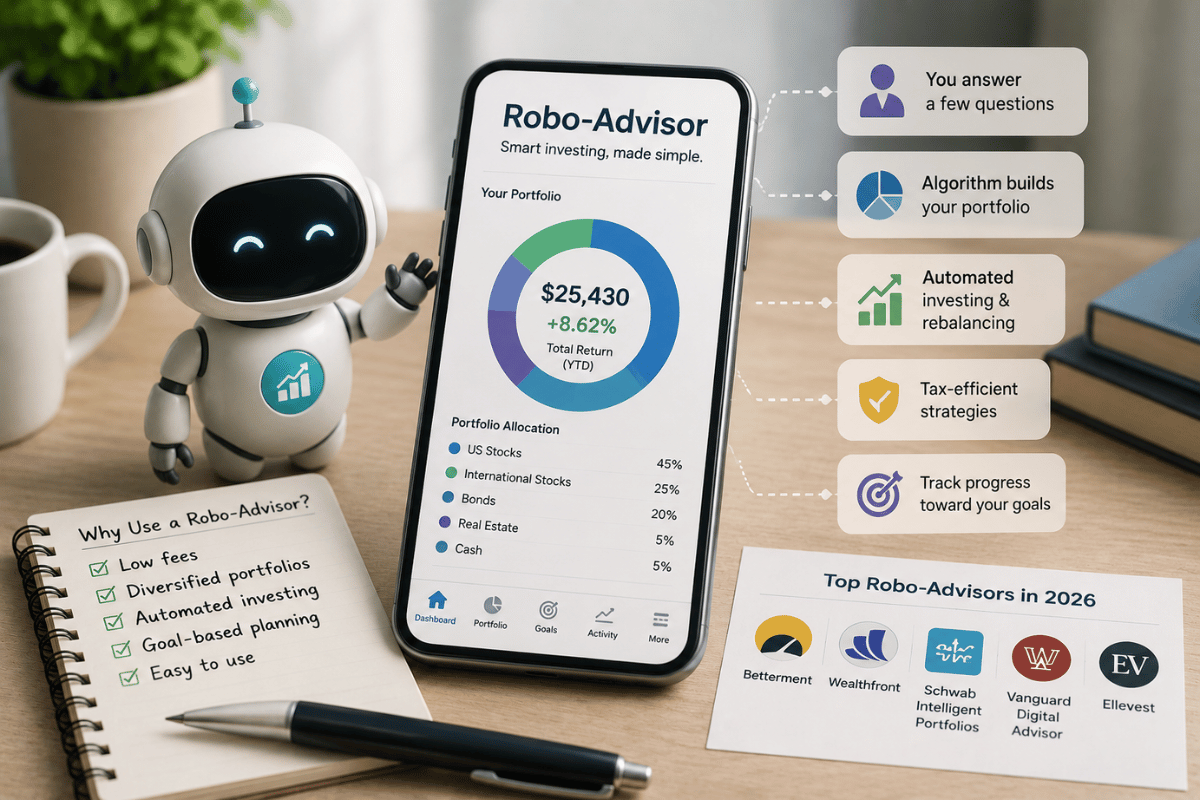

A robo-advisor is an automated digital platform that builds and manages an investment portfolio on your behalf using algorithms. You answer a short questionnaire about your financial goals, investment timeline, and risk tolerance. The platform then creates a diversified portfolio, usually made up of low-cost index funds or exchange-traded funds (ETFs), and automatically manages it over time.

The management includes rebalancing your portfolio when market movements shift your asset allocation away from your target, and in many cases, tax-loss harvesting, which is a strategy that reduces your tax bill by selling investments that have declined in value to offset gains elsewhere.

You do not need to make any investment decisions yourself. The algorithm handles everything according to the parameters you set up when you joined.

How Does a Robo-Advisor Actually Work?

Step 1: Onboarding Questionnaire

When you sign up, the platform asks questions such as: What are you investing for? When will you need the money? How would you feel if your portfolio dropped 20% in value? Your answers feed into an algorithm that determines your investor profile.

Step 2: Portfolio Construction

Based on your profile, the algorithm selects a mix of asset classes: typically domestic stocks, international stocks, bonds, and sometimes real estate investment trusts (REITs) or commodities. Most robo-advisors use passive index funds rather than actively managed funds, which keeps costs low.

Step 3: Automatic Rebalancing

Markets move constantly. If stocks rise significantly, your portfolio might drift from a 70% stock / 30% bond allocation to 80% / 20%. The robo-advisor automatically sells some stock and buys bonds to bring you back to your target allocation. This happens without any action from you.

Step 4: Tax-Loss Harvesting (Premium Feature)

Many robo-advisors offer tax-loss harvesting, which involves selling investments that have fallen in value to realise a capital loss. That loss can then be used to offset taxable gains elsewhere in your portfolio, reducing your tax liability. This feature is typically available on larger account balances or higher-tier plans.

Robo-Advisor vs Human Financial Advisor: Key Differences

| Factor | Robo-Advisor |

| Annual fee | 0.15% to 0.50% of assets |

| Minimum investment | $0 to $500 typically |

| Personalisation | Algorithm-based, standardised |

| Tax-loss harvesting | Automated (most platforms) |

| Human contact | Limited or none (varies) |

| Best for | Straightforward goals, passive investors |

| Not ideal for | Complex tax situations, estate planning |

| Factor | Human Financial Advisor |

| Annual fee | 0.8% to 1.5% of assets, or flat fee |

| Minimum investment | Often $50,000 to $250,000+ |

| Personalisation | Fully customised to your situation |

| Tax-loss harvesting | Manual, tailored strategy |

| Human contact | Regular meetings and calls |

| Best for | Complex finances, life transitions |

| Not ideal for | Small portfolios (fees eat returns) |

The Main Advantages of Robo-Advisors

- Low cost: Management fees of 0.15% to 0.50% per year are far lower than the 0.8% to 1.5% typically charged by human advisors. On a $50,000 portfolio, this difference saves $325 to $675 per year.

- No minimum barrier: Most platforms let you start with as little as $1 to $500, making investing accessible to beginners.

- Fully automated: You set up your account once and the platform handles everything. No need to monitor markets or make decisions.

- Emotionless investing: Algorithms do not panic during market downturns or get greedy during rallies. They maintain your strategy regardless of short-term market movements.

- Diversification by default: Your money is spread across hundreds or thousands of individual securities through index funds, reducing single-stock risk.

- Tax efficiency: Automated tax-loss harvesting can improve after-tax returns, particularly for higher earners.

The Limitations of Robo-Advisors

- Limited personalisation: Algorithms cannot account for complex personal circumstances such as inheritance, business income, divorce settlements, or unusual tax situations.

- No human relationship: When markets crash and emotions run high, many investors benefit from a human advisor who can talk them off the ledge. Robo-advisors cannot provide that emotional guidance.

- Standardised portfolios: Most platforms offer a relatively small number of portfolio options. You cannot customise individual holdings.

- Not suitable for active traders: Robo-advisors are designed for long-term, passive investing. If you want to pick individual stocks or trade frequently, they are not the right tool.

Leading Robo-Advisors in 2026: A Comparison

Below is a summary of the main robo-advisor platforms available in 2026. Always verify current fees and features directly with each provider, as these change over time.

| Platform | Annual Fee | Notable Feature |

| Betterment | 0.25% (0.40% premium) | Tax-loss harvesting, socially responsible option |

| Wealthfront | 0.25% | Direct indexing at $100k+, financial planning tools |

| Vanguard Digital Advisor | approx. 0.15% | Ultra-low cost, strong for retirement accounts |

| Schwab Intelligent Portfolios | 0% management fee | No fee, but requires 6-10% cash allocation |

| Ellevest | 0.25% monthly | Designed specifically for women’s financial goals |

| M1 Finance | 0% (M1 Premium available) | Hybrid: automated plus self-directed investing |

Note: Fees listed are management fees and do not include the underlying fund expense ratios, which typically add 0.03% to 0.15% on top.

Who Should Use a Robo-Advisor?

A robo-advisor is an excellent choice if:

- You are a beginner investor and want to start without needing to learn portfolio construction

- You have straightforward financial goals such as building a retirement fund or saving for a house deposit

- You have a small to medium portfolio size where a human advisor’s fees would consume too much of your returns

- You want a fully hands-off approach and prefer not to make ongoing investment decisions

- You tend to make emotional decisions during market volatility and want a system that keeps you disciplined

Who Should NOT Use a Robo-Advisor?

- People with complex financial situations: business owners, those with significant inheritance, or people navigating major life transitions

- High-net-worth individuals who need bespoke tax planning, estate planning, or trust management

- Active traders who want control over individual stock or fund selection

- People who need regular human contact and reassurance during market downturns

Frequently Asked Questions

Is my money safe with a robo-advisor?

Yes, for regulated platforms. In the US, most robo-advisors are registered investment advisers and hold client assets at SIPC-insured broker-dealers, protecting up to $500,000 per account in the event of broker failure. In the UK, platforms are regulated by the FCA and covered by the Financial Services Compensation Scheme up to £85,000. Robo-advisors do not protect against investment losses from market movements, which is normal for any investment.

Can a robo-advisor beat the market?

Most do not try to. Robo-advisors typically use passive index funds that aim to match market returns, not beat them. Research consistently shows that most actively managed funds fail to outperform their benchmark index over a 10-year period after fees. Matching the market at very low cost is a sound long-term strategy for most investors.

What happens to my money if the robo-advisor company shuts down?

Your investments are held separately from the company’s own assets at a custodian bank or brokerage. If the robo-advisor company closes, your investments are returned to you or transferred to another provider. This is different from keeping cash at a bank. The custody structure is designed specifically to protect client assets.

How much money do I need to start?

Many robo-advisors have no minimum investment, including Betterment and Ellevest. Others require a modest minimum of $100 to $500. Schwab requires $5,000 for its Intelligent Portfolios product. Starting small is perfectly fine; the habit of regular contributions matters more than the starting amount.

Are robo-advisors better than index funds I manage myself?

For disciplined investors who are comfortable managing their own portfolio, buying index funds directly through a brokerage is slightly cheaper. The value of a robo-advisor is largely behavioural: it removes the temptation to time the market, handles rebalancing automatically, and lowers the barrier to getting started. For many people, that is worth the small fee difference.

Key Takeaways

| Summary: What Is a Robo-Advisor?A robo-advisor builds and manages an investment portfolio automatically using algorithms.You answer a questionnaire; the platform does the rest, including rebalancing and tax-loss harvesting.Fees are typically 0.15% to 0.50% per year, far lower than human advisors.Best suited to beginner and passive investors with straightforward goals.Not ideal for complex financial situations that require personalised human advice.Your money is held at regulated custodians and is protected up to legal limits. |

Robo-advisors are not the right tool for everyone, but for many people they represent the simplest, cheapest, and most disciplined entry point into long-term investing. If your goal is to grow wealth steadily over time without making it a part-time job, a robo-advisor is worth serious consideration.

Disclaimer

The content on Next Future Finance is for informational and educational purposes only and does not constitute financial, investment, or legal advice. Always consult a qualified financial professional before making any financial decisions. Individual results may vary.