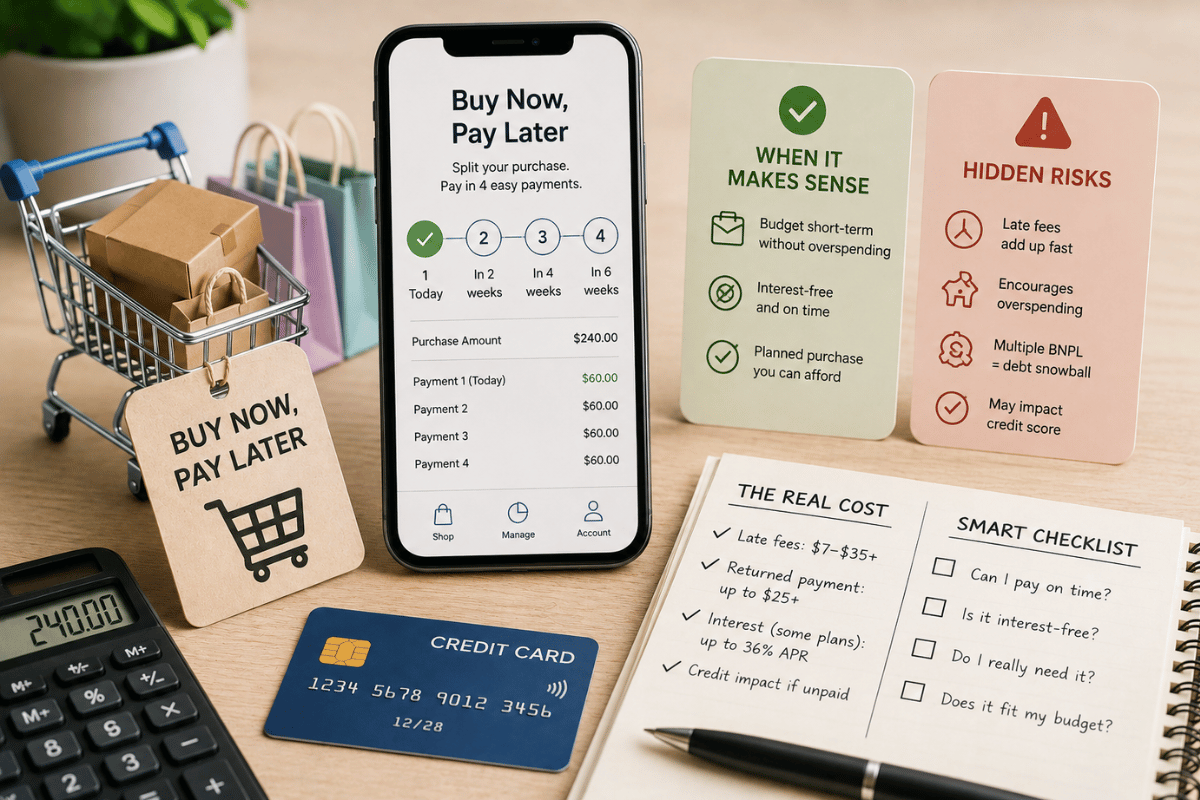

Buy Now Pay Later has exploded in popularity over the last five years. Services like Klarna, Afterpay, Affirm, and dozens of competitors have made it possible to split almost any purchase into instalments with a tap of your phone.

On the surface, it sounds like a better credit card: no interest, flexible payments, instant approval. But BNPL is not free money. Used carelessly, it can lead to missed payments, debt accumulation, damaged credit, and a distorted sense of what you can actually afford.

This guide explains exactly how BNPL works, what it really costs you, the risks most providers do not advertise, and the specific situations where it genuinely makes financial sense.

How Buy Now Pay Later Works

BNPL is a short-term financing option offered at the point of sale, either online or in-store. Instead of paying the full price immediately, you split the cost into equal instalments paid over weeks or months.

The most common structure is Pay in 4: you pay 25% immediately and the remaining 75% in three equal payments every two weeks. This structure is typically interest-free if all payments are made on time.

Longer-term BNPL products, typically offered for higher-value purchases, can extend repayment over 6, 12, or 24 months. These often carry interest rates, sometimes as high as 29.99% APR, which is comparable to or higher than many credit cards.

| BNPL Structure | How It Works |

| Pay in 4 | Split into 4 payments every 2 weeks. Usually 0% interest if on time. |

| Pay in 3 | 3 equal monthly payments. Often 0% interest. |

| 6 to 24 month plans | Monthly payments with interest, often 10% to 30% APR. |

| Pay in 30 days | Pay the full amount within 30 days. No interest if paid in time. |

The Real Cost of Buy Now Pay Later

When It Is Truly Free

A Pay in 4 plan from a major provider, where you make all payments on time, genuinely costs nothing extra. You pay exactly what you would have paid upfront. This is the scenario BNPL companies advertise and it is accurate for disciplined users.

Late Payment Fees

Miss a payment and the cost picture changes immediately. Late fees vary by provider but typically range from $5 to $15 per missed payment. For a $100 purchase split into four $25 payments, a $10 late fee on one instalment represents a 40% penalty on that payment.

Interest on Longer Plans

If you use a 12-month or 24-month BNPL plan for a larger purchase, interest applies from the first payment. A $1,200 laptop financed over 12 months at 24.99% APR costs approximately $173 in interest, bringing the total to $1,373. That same laptop on a 0% credit card introductory offer would cost nothing extra.

| Real Cost Example: $800 Purchase Pay in 4 (all on time): $800 total (0% extra cost) Pay in 4 (one late payment): $815 total ($15 late fee) 12-month plan at 24.99% APR: $909 total ($109 interest) 24-month plan at 29.99% APR: $1,056 total ($256 interest) |

Returned Items Complications

Returning a BNPL purchase is more complicated than returning something paid by card. While most providers process refunds, you typically must continue making payments while the return is being processed. In some cases, providers may not refund fees already charged. Disputes take longer to resolve than standard credit card chargebacks.

How BNPL Affects Your Credit Score

This is one of the most misunderstood aspects of Buy Now Pay Later. The impact on your credit depends heavily on the provider and the plan type.

Soft vs Hard Credit Checks

Most Pay in 4 plans use a soft credit check, which does not affect your credit score. Longer-term financing plans often require a hard credit check, which can reduce your score by a few points.

Reporting to Credit Bureaus

Whether BNPL activity appears on your credit report depends on the provider. Some providers now report payment history to credit bureaus, which means on-time payments can help your score and missed payments can hurt it. The reporting landscape has become more consistent in 2025 and 2026 as regulators have pushed for greater transparency.

Debt-to-Income and Affordability Assessment

Even if a BNPL plan does not appear on your credit report, some mortgage and loan lenders now ask about BNPL commitments during affordability assessments. Having multiple active BNPL plans can affect your ability to get approved for other credit products.

Hidden Risks Most BNPL Users Overlook

Spending More Than You Would Otherwise

This is the central risk. Research consistently shows that BNPL users spend more per transaction than those paying upfront. When a $240 purchase becomes four $60 payments, it feels psychologically affordable even if your budget cannot genuinely support it. BNPL is designed to reduce the psychological friction of spending.

Multiple Plans Stacking Up

Because each BNPL plan feels small, it is easy to accumulate several at once without realising the total commitment. Four separate plans at $50 per fortnight each equals $200 per fortnight in obligations that may not appear in your regular budget tracking.

Inconsistent Consumer Protections

Credit cards in most countries offer strong consumer protections including charge-back rights, fraud protection, and Section 75 protection in the UK. BNPL has historically had weaker protections, though regulation has been increasing. Always check what recourse you have if a product is faulty or a merchant does not deliver.

Debt Cycle Risk

For users who struggle with cash flow, using BNPL to cover purchases they cannot afford today simply moves the problem to next month. If the payment falls due during a tight pay period, the choice becomes: pay the BNPL or pay a bill. This is the beginning of a debt cycle.

Major BNPL Providers in 2026: A Comparison

| Provider | Main Structure | Late Fee |

| Klarna | Pay in 4, Pay in 30, Financing | Up to $35 |

| Afterpay / Clearpay | Pay in 4 | $10, max 25% of order |

| Affirm | Pay in 4, 6-24 month plans | No late fee, but interest accrues |

| PayPal Pay Later | Pay in 4, Pay in 6 months | No late fee |

| Zip (Quadpay) | Pay in 4 | $5 to $10 per late payment |

| Apple Pay Later (US) | Pay in 4 | No late fee |

Always read the full terms of any BNPL plan before agreeing. Fee structures, credit reporting policies, and dispute processes vary significantly.

When BNPL Actually Makes Financial Sense

BNPL is not inherently bad. Used in the right circumstances, it is a genuinely useful tool. Here are the situations where it makes sense:

- Cash flow timing mismatch: You have a paycheck arriving in two weeks but need to buy something necessary today. Pay in 4 at 0% is a free short-term bridge.

- Interest-free purchase you budgeted for: You were going to buy this item anyway, you have the full amount set aside, and splitting the payments costs nothing. The money earns interest sitting in your account.

- Large necessary purchase with 0% financing: A 0% BNPL plan on a needed appliance or laptop that you would otherwise put on a high-interest card is a smarter choice.

- Building purchase history without a credit card: For those building credit, some BNPL providers now report to credit bureaus. Using BNPL responsibly can contribute to a credit profile.

When to Avoid BNPL

- Impulse purchases: If you would not buy it with cash today, BNPL is masking an affordability problem, not solving one.

- Items you might return: The refund and dispute process is slower and more complicated than credit cards.

- When you have existing BNPL plans: Multiple simultaneous plans dramatically increase the risk of a missed payment.

- Long-term plans with interest: Any BNPL product with an APR above your credit card rate is an expensive form of financing.

- When you are already in debt: Adding BNPL obligations to an already stretched budget is a risk not worth taking.

Frequently Asked Questions

Is Buy Now Pay Later bad for your finances?

It depends entirely on how you use it. For a disciplined user who only uses Pay in 4 on budgeted purchases, makes all payments on time, and never accumulates multiple plans simultaneously, BNPL is neutral to mildly positive. For impulsive spenders or people with tight budgets, it is a genuine financial risk.

Can BNPL affect a mortgage application?

Yes. Even if BNPL plans are not on your credit report, some mortgage lenders ask applicants to disclose all monthly financial commitments. Active BNPL plans reduce your disposable income and can affect your borrowing capacity. It is advisable to close all BNPL plans before applying for a mortgage.

What happens if I cannot make a BNPL payment?

Most providers will charge a late fee and attempt to collect the payment on the next scheduled date. If payments remain missed, the account may be sent to collections, which will appear on your credit report. Contact the provider as soon as you know you cannot pay; most have hardship provisions.

Is BNPL regulated?

Regulation has increased significantly in 2025 and 2026 in most major markets. In the UK, the Financial Conduct Authority introduced formal BNPL regulation in 2024 requiring affordability checks and clearer disclosure. In the US, the Consumer Financial Protection Bureau has classified BNPL providers as credit card issuers for regulatory purposes. Check the current regulatory status in your country.

Key Takeaways

| Summary: Buy Now Pay Later BNPL splits purchases into instalments, typically 4 payments over 6 weeks. Pay in 4 plans are genuinely free if all payments are made on time. Late fees, interest on longer plans, and overspending are the three main financial risks. Multiple simultaneous BNPL plans are a common and underestimated danger. BNPL can affect mortgage applications even if not on your credit report. Use it only for budgeted purchases where the 0% structure provides a genuine advantage. |

BNPL is a tool. Like any financial tool, its value depends on how you use it. Understand the terms before you commit, never use it to buy something you cannot genuinely afford, and always track your active plans as part of your monthly budget.

Disclaimer

The content on Next Future Finance is for informational and educational purposes only and does not constitute financial, investment, or legal advice. Always consult a qualified financial professional before making any financial decisions. Individual results may vary.