I grew up in a family where money was always tight. My parents worked incredibly hard, but like so many normal families, they lived paycheck to paycheck. There was love, there was sacrifice, but there was rarely any financial cushion — and certainly no talk of building something that could last beyond their lifetime.

That reality shaped me deeply. When I had my own children, I made a quiet promise: I didn’t want them to grow up with the same constant financial anxiety I felt. I wanted to build something more stable — not just for them, but for their children too.

Over the years, I’ve learned that generational wealth isn’t about getting rich quick or having a perfect six-figure income. It’s about making consistent, intentional decisions that compound over time. And in today’s world, with AI tools, better access to information, and new investment opportunities, normal families actually have a real shot at doing this.

This isn’t theory. These are the practical strategies that have worked in my own life and in the lives of many ordinary families I’ve spoken with.

What Generational Wealth Really Means

Generational wealth isn’t just a big bank account. It’s the combination of financial assets, knowledge, habits, and opportunities that get passed down.

It means your children won’t have to start from zero. It means they can focus on their passions instead of just surviving. It means your grandchildren inherit not only money, but also the wisdom of how to manage it.

For most normal families, this journey starts with three things:

- Changing how you think about money

- Building strong financial habits

- Making smart, consistent investments in assets that grow over decades

The good news? You don’t need to be a high earner or a financial genius to begin.

Strategy 1: Build a Strong Foundation with Habits That Compound

The most powerful thing any normal family can do is develop consistent habits.

I started small. My wife and I committed to living below our means — not in a restrictive, joyless way, but with intention. We automated savings the day we got paid. We treated our future selves like important family members who deserved to be paid first.

We also focused on education — not formal degrees, but real financial literacy. We read books together, discussed money openly with our kids (in age-appropriate ways), and made it normal to talk about budgeting, investing, and delayed gratification.

One of the best decisions we made was creating a “Family Wealth Book” — a simple document where we track our net worth, goals, and lessons learned. Every year we review it together. It has become one of our most valuable family assets.

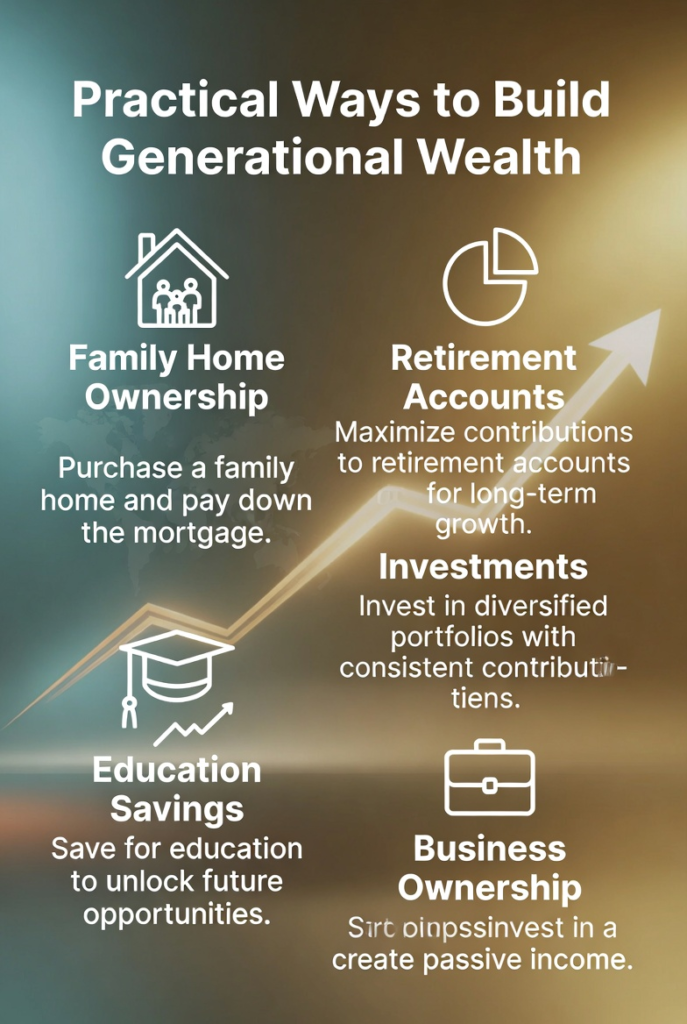

Strategy 2: Invest in Assets That Grow Over Generations

Real generational wealth comes from owning assets, not just earning income.

For normal families, this often starts with:

- Your home — buying a house you can afford and paying it down steadily

- Retirement accounts — maxing out tax-advantaged accounts like 401(k)s and IRAs

- Index funds and broad market investments — low-cost, diversified funds that grow with the economy

- Education funds for children — 529 plans or similar vehicles

I personally allocate a portion of our investments into real assets — things that hold value over time like real estate (even through REITs if direct ownership isn’t possible) and businesses.

AI tools have made this much easier. I now use AI to analyze opportunities, run long-term projections, and keep our portfolio balanced without needing expensive advisors.

Strategy 3: Protect What You Build and Pass Down Wisdom

Wealth that disappears in one generation isn’t generational wealth.

This is why we focus heavily on:

- Proper insurance (life, health, disability)

- Estate planning — even simple wills and beneficiary designations

- Teaching financial responsibility to our children through real experiences

We involve our kids in age-appropriate money decisions. They have small investment accounts they help manage. They learn by doing — and by watching us.

One of the most important things we’ve done is write letters to our children explaining our values around money, work, and family. These letters will be given to them when they turn 18 and 25. They contain no financial advice — just the “why” behind our choices.

Strategy 4: Leverage Technology and New Opportunities

We’re living in a unique time. AI, automation, and new investment vehicles are making wealth building more accessible than ever.

I use AI regularly to:

- Optimize our taxes

- Find better savings and investment rates

- Model different financial scenarios for the next 10–30 years

- Learn about emerging opportunities like tokenized assets

But technology is only a tool. The real work is still human — discipline, patience, and love for your family.

The Most Important Truth

Building generational wealth is a marathon, not a sprint. There will be setbacks. Markets will crash. Life will throw curveballs.

What matters is staying consistent, staying humble, and keeping your family’s future at the center of your decisions.

You don’t need to be perfect. You just need to start — and keep going.

If you’re a normal family reading this, I want you to know it’s possible. My own journey started from very little, and we’re still far from “done.” But every month, every year, we’re moving forward.

Your children and grandchildren will thank you — not just for the money, but for the example you set and the opportunities you created.

Written by Dhanur