Your credit score is one of the most important numbers in your financial life. It determines whether you get approved for a loan, what interest rate you pay on a mortgage, whether a landlord accepts your rental application, and sometimes even whether an employer hires you.

Yet most people have only a vague idea of what their credit score actually is, how it is calculated, or what moves the needle. This guide changes that. By the end, you will know exactly where your score comes from, what damages it, and what you can do right now to improve it.

What Is a Credit Score?

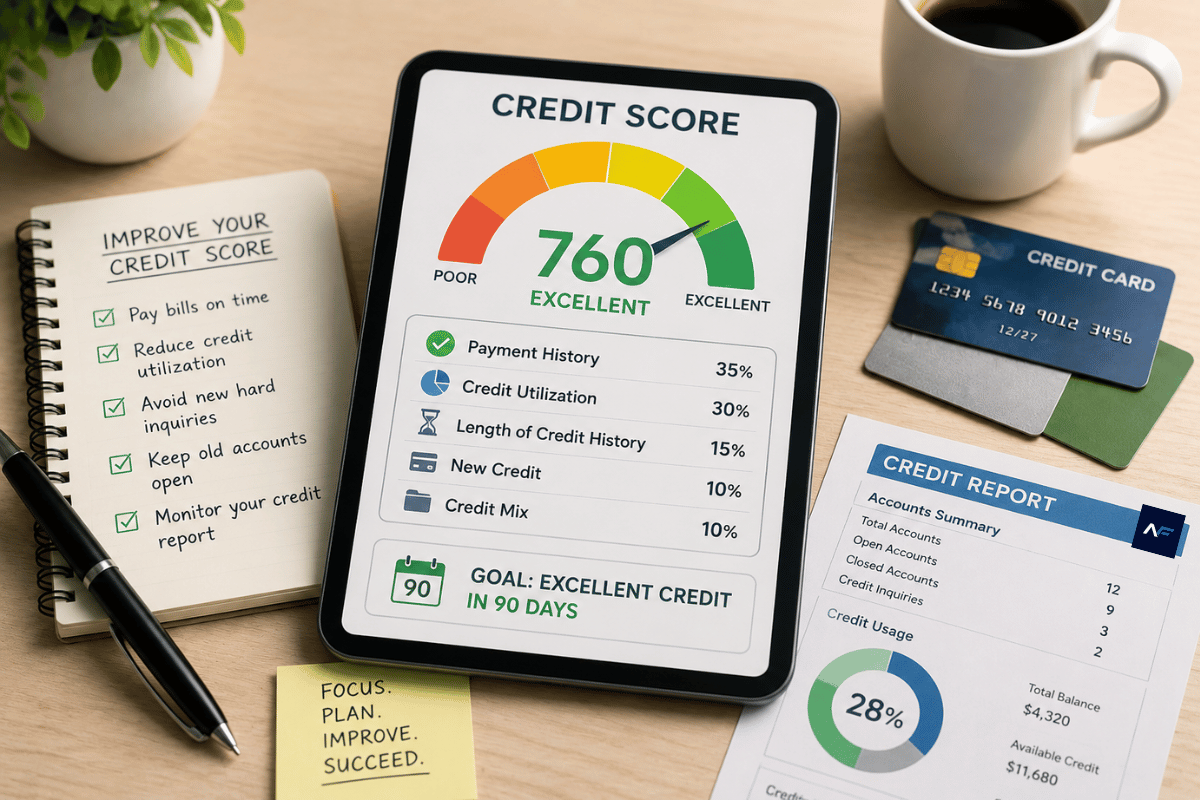

A credit score is a three-digit number, typically ranging from 300 to 850, that summarises your creditworthiness based on your borrowing and repayment history. Lenders use it to quickly assess how likely you are to repay a debt on time.

The most widely used scoring model is the FICO Score, developed by the Fair Isaac Corporation. VantageScore is another common model used by some lenders and free credit monitoring services. Both use a 300 to 850 range and evaluate similar factors, though with slightly different weightings.

Your score is generated from information held in your credit report, which is maintained by the three major credit bureaus: Equifax, Experian, and TransUnion. Because each bureau may hold slightly different information, your score can vary slightly between them.

| Score Range | Rating |

| 800 to 850 | Exceptional |

| 740 to 799 | Very Good |

| 670 to 739 | Good |

| 580 to 669 | Fair |

| 300 to 579 | Poor |

Why Your Credit Score Matters

A higher credit score unlocks better financial terms across nearly every area of life. Here is a practical illustration of what the difference looks like in real money:

| Scenario | Impact |

| Mortgage (30-year, $300,000) | Difference of 1.5% APR = approx. $90,000 more paid over loan lifetime |

| Car loan ($25,000) | Fair vs. excellent score = $3,000 to $5,000 more in total interest |

| Credit card APR | Poor credit = 24-29% APR vs. 12-15% with good credit |

| Rental application | Many landlords require a minimum score of 620 to 650 |

| Insurance premiums | Lower scores can increase premiums by 20 to 50% in some regions |

The 5 Factors That Determine Your Credit Score

FICO calculates your score using five factors, each weighted differently. Understanding these is essential because every action that improves or damages your score connects back to one of them.

1. Payment History (35%)

This is the single most important factor. It records whether you have paid your bills on time. A single missed payment can drop your score by 50 to 100 points. Late payments stay on your report for up to seven years, though their impact fades over time.

What damages payment history: missed payments, accounts sent to collections, bankruptcies, foreclosures, and charge-offs.

2. Amounts Owed / Credit Utilisation (30%)

This measures how much of your available credit you are currently using. It is calculated as your total credit card balances divided by your total credit limits.

A utilisation rate below 30% is considered good. Below 10% is ideal for the highest scores. Maxing out your credit cards, even if you pay them off monthly, can temporarily hurt your score if the balance is reported before you pay.

| Credit Utilisation ExampleTotal credit limits across all cards: $10,000Current balances: $2,800Utilisation rate: 28% (Good) If balance rises to $5,500:Utilisation rate: 55% (Damaging) |

3. Length of Credit History (15%)

The longer your credit history, the better. This factor considers the age of your oldest account, the age of your newest account, and the average age of all accounts. This is why closing old credit cards can hurt your score even if you do not use them.

4. Credit Mix (10%)

Lenders like to see that you can responsibly manage different types of credit. Having a mix of revolving credit (credit cards) and instalment loans (mortgages, car loans, student loans) positively affects this factor. You should not open accounts purely to improve your mix, but it is worth understanding why having only one type can limit your score.

5. New Credit / Hard Enquiries (10%)

Every time you apply for new credit, a hard enquiry is recorded on your report. Multiple hard enquiries in a short period signal financial stress to lenders and can lower your score by a few points each. Soft enquiries, such as checking your own score or a lender doing a background check without your application, do not affect your score.

What Damages Your Credit Score: The Most Common Causes

- Missing a payment: The most damaging single event. Even one missed payment can drop your score by 50 to 100 points.

- High credit utilisation: Using more than 30% of your available credit limit, especially across multiple cards.

- Closing old accounts: Reduces your average account age and total available credit, both of which can lower your score.

- Applying for multiple loans or cards at once: Multiple hard enquiries in a short window signal desperation to lenders.

- Collections and charge-offs: Unpaid debts sent to collections stay on your report for seven years.

- Bankruptcy: Chapter 7 bankruptcy stays on your report for 10 years. Chapter 13 stays for 7 years.

- Errors on your credit report: Incorrect information from lenders or identity theft can lower your score unfairly.

Your 90-Day Credit Score Improvement Plan

You cannot repair credit overnight, but consistent action over 90 days produces measurable results. Here is a week-by-week plan.

Days 1 to 7: Get a Clear Picture

Pull your credit reports from all three bureaus. In the US, you can do this for free at AnnualCreditReport.com. In the UK, use Experian, Equifax, or TransUnion directly. Check every account for errors: incorrect balances, accounts you did not open, payments marked late that were on time.

Dispute any errors immediately. Write to the credit bureau in question with evidence. Bureaus are legally required to investigate and respond within 30 days in most jurisdictions.

Days 8 to 30: Fix the Foundations

- Set up automatic minimum payments on every account so you never miss a due date again

- Pay down any card that is above 30% utilisation, starting with the highest utilisation card first

- Do not close any old accounts, even ones you do not use

- Avoid applying for any new credit during this period

Days 31 to 60: Accelerate the Gains

Focus extra money on reducing balances. Even moving from 55% utilisation to 30% on one card can add 20 to 40 points. If you have a card with a $3,000 balance and a $5,000 limit, paying it down to $1,500 moves utilisation from 60% to 30%.

If you have a thin credit file (few accounts or short history), consider asking a trusted family member to add you as an authorised user on one of their older, well-managed cards. You benefit from their account’s history without needing to spend on the card.

Days 61 to 90: Maintain and Monitor

By now, disputes should be resolved, utilisation should be lower, and automatic payments should be in place. Your score will be climbing.

- Check your score monthly using a free monitoring tool

- Keep utilisation below 30% as a permanent habit

- Continue paying every account on time, every month

- Only apply for new credit when genuinely needed

| Action | Expected Score Impact |

| Correcting a credit report error | 10 to 100+ points depending on the error |

| Reducing utilisation from 60% to under 30% | 20 to 50 points |

| Adding an on-time payment record for 3 months | 5 to 20 points |

| Removing a collections account (paid or disputed) | Up to 100 points |

| Becoming an authorised user on a good account | 10 to 40 points |

Frequently Asked Questions

How long does it take to build credit from scratch?

Most people can establish a basic credit score within three to six months of opening their first credit account. Building a strong score (above 700) typically takes one to two years of consistent, on-time payments and responsible usage.

Does checking my own credit score lower it?

No. Checking your own score is called a soft enquiry and has no impact on your score whatsoever. Only hard enquiries from lenders processing an application affect your score.

How long do negative items stay on my credit report?

Most negative items, including late payments, collections, and charge-offs, remain on your report for seven years from the date of the first missed payment. Bankruptcies remain for seven to ten years depending on the type. Positive information, such as well-managed accounts, can stay much longer.

Can I improve my score if I have no credit history?

Yes. Options include applying for a secured credit card (where you deposit cash as collateral), becoming an authorised user on a family member’s account, or taking out a credit-builder loan from a credit union. Use these tools consistently and your score will build over time.

Does income affect my credit score?

No. Income is not a factor in any credit scoring model. However, lenders do consider your income separately when evaluating loan applications, as it determines your ability to repay independent of your creditworthiness.

Should I pay off debt or keep accounts open?

Both. Pay down balances to reduce utilisation, but keep the accounts open to preserve your credit history length and available credit. The only reason to close an account is if it charges an annual fee that outweighs any benefit.

Key Takeaways

| Summary: Credit Score ExplainedYour credit score ranges from 300 to 850. Above 670 is good; above 740 is very good.Payment history (35%) and credit utilisation (30%) are the two biggest factors.Keep utilisation below 30% and pay every bill on time, every month.Never miss a payment. A single late payment can drop your score by 50 to 100 points.Check your credit report for errors and dispute anything that is incorrect.90 days of consistent action produces measurable improvement in most cases. |

Your credit score is not a fixed verdict on your financial life. It is a live number that responds to your behaviour. The actions you take this month will show up in your score within 30 to 60 days. Start today, stay consistent, and the improvement will come.

Disclaimer

The content on Next Future Finance is for informational and educational purposes only and does not constitute financial, investment, or legal advice. Always consult a qualified financial professional before making any financial decisions. Individual results may vary.